SEE UPDATED POST, AUGUST 11, 2019: Trump Administration Labels China a “Currency Manipulator”: What’s behind the accusation, and who’s right?

© 2016 Prof. Farok J. Contractor, Rutgers Business School

This article is a 2016 update of my original post of November 16, 2015. It has also been published on The Conversation as Does China manipulate its currency as Donald Trump claims? on June 13, 2016. Subsequently, it was also picked up by USNews.com on June 22, 2016, as Does China Manipulate its Currency Like Donald Trump Says? Countries have multiple ways to “manage” their currencies to some degree.

After 20 years, the Chinese government must be used to it—being bashed by US politicians and Congress as a “currency manipulator.” Indeed, the exchange value of the yuan (or renminbi [RMB]) is fixed each morning by its central bank, the People’s Bank of China (PBoC), with a narrow band of only + 2 percent allowed, up or down, within which market forces can have their say. In effect, it is an exchange rate set and controlled by the PBoC.

But why pick on just China?

Most countries “manipulate” their exchange rates…

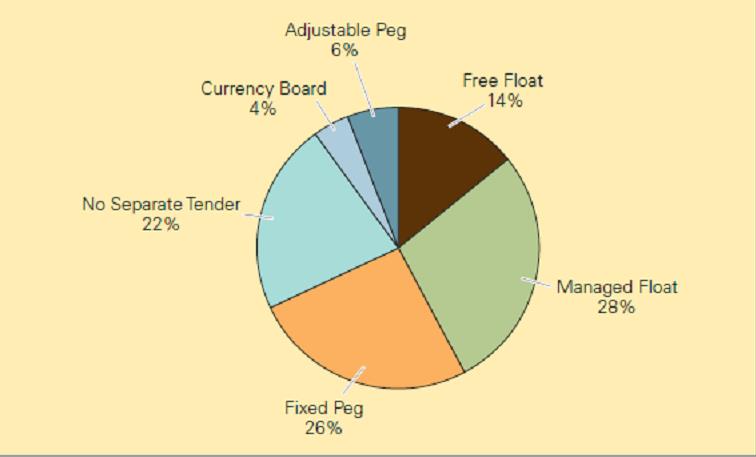

According to the IMF (International Monetary Fund), well over half its member countries’ governments meddle, in a mild or total fashion, to influence or fix their exchange rates, as illustrated in Figure 1.

Figure 1: IMF member nations intervene in foreign exchange rates by various means (Source: IMF)

“Fixed Peg” and “Currency Board” countries have currency values fixed for a considerable period of months or years. In “Managed Float” cases, market forces are allowed to play, but with the government intervening (buying or selling) to bias the exchange rate upward or downward. “Adjustable Pegs” are situations where the government fixes the rate temporarily—for months at a time or daily, as in the case of China. It is only with a few major currencies, such as the dollar or euro, that the government allows a “Free Float” with minimal or no intervention.

What exactly is behind the accusation of “currency manipulation”?

Generally, the accusation alleges that the government is keeping its currency too weak, overly devalued, or undervalued in order to give an artificial boost to exports while keeping out imports. This has the effect of boosting jobs in that country.

Take China as an example. A Chinese exporter earning a dollar in mid-2016 turns it into the bank and gets around 6.5 RMB yuan. By comparing costs in China and elsewhere, IMF and other economists calculate a hypothetical purchasing power parity (PPP) rate of 5.7 RMB/$, which would supposedly prevail under market equilibrium and without government meddling.[1] At 6.5 in mid-2016, some economists argue the RMB is still undervalued. But if the theoretical rate of 5.7 RMB/$ were to happen, the Chinese exporter would get only 5.7 RMB per dollar at the bank counter. The 6.5 RMB/$ actual mid-2016 rate provides a 14 percent higher revenue to the Chinese exporter, compared with the hypothetical 5.7 RMB/$ rate that some economists say should prevail. The still-undervalued 6.5 RMB/$ rate, they allege, gives the Chinese exporter an advantage.

By the same token, imports into China cost 14 percent more at the allegedly undervalued 6.5 RMB/$ rate than at the PPP 5.7 RMB/$. This, they allege, makes imports into China 14 percent more expensive than they should be, thereby keeping some foreign products out of China and benefiting (or protecting) Chinese firms that produce substitute products that compete with imports. On both the import and export side, an undervalued exchange rate boosts or preserves jobs in China (at the expense of jobs in the rest of the world).

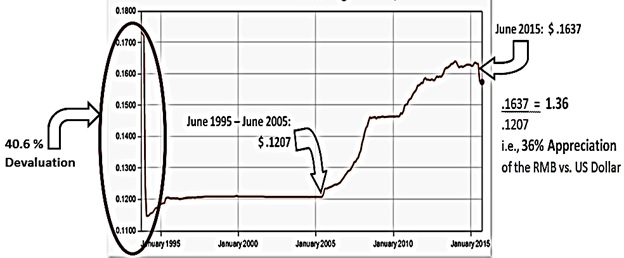

But the Chinese have already massively appreciated their currency since 2005…

It must be particularly galling to the Chinese to hear accusations of currency manipulation since, succumbing to pressure from Western countries, they have already massively appreciated their currency in the 10 years since 2005. In June 2005, following more than a decade of a fixed exchange rate of 8.27 RMB/$ (when it was indeed undervalued), the Chinese gradually appreciated their currency all the way to 6.2 RMB/$ by July 2015. In the minds of many Chinese economists, their currency is no longer undervalued in the range of 6.2–6.5 because of three reasons:

1. Between June 2005 and July 2015, the RMB appreciated/strengthened by 36 percent

This 10-year climb, as shown in Figure 2a, means that Chinese exporters in 2015 earned as much as 33 percent less that they would have at the 2005 exchange rate. Several Chinese exporters found themselves uncompetitive with the stronger currency and had to shut down their operations in China and relocate production to Vietnam, Bangladesh, or Africa.

Figure 2a: China’s RMB exchange rate history—a decade of climbing was followed by a reversal (Source: Wall Street Journal, May 23, 2016)

Also, imports into China costing 33 percent less in 2015 than in 2005 means that some Chinese domestic production was displaced by import competition.

In both cases, the appreciation of the yuan (RMB) has meant reduction of jobs in China, although this is consistent with the peaking of the Chinese labor force (partially as a consequence of the one-child policy). Indeed, labor shortages exist in several areas in China.

Going even farther back into the first half of the 1990s, we see in Figure 2b that the yuan had been massively devalued by more than 40% by the Deng Xiaoping-led government in order to jump-start the Chinese export engine and make China the “factory of the world.” But by 2015/2016, with the 10-year appreciation of the currency, the RMB had more or less regained its value compared with the early 1990s.

Figure 2b: Going farther back, note the huge devaluation of the RMB in the early 1990s (Source: Oanda.com)

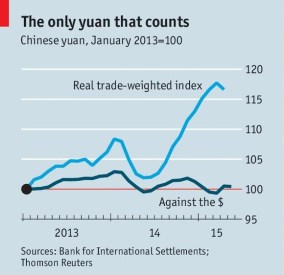

2. The yuan (RMB) has appreciated even more against other currencies

The PBoC has fixed the RMB only against the US dollar. But since 2013, this means that as the dollar has risen against most other currencies (e.g., the euro, emerging-country currencies such as the Brazilian real), the RMB has appreciated or strengthened even more, piggybacking on the dollar; see Figure 3.

Figure 3: The yuan has (reluctantly) piggybacked on the US dollar

(Source: The Economist, May 30, 2015)

If one combines the RMB appreciation shown in Figure 2b (36 percent) with the dollar’s appreciation against most other currencies since 2013 (15 percent), the local currency cost of importing Chinese products may have risen by more than 50 percent since 2005 for many prospective buyers in a large swathe of nations from Europe to Brazil.

3. Chinese wage and cost inflation

On the east coast of China, where most of its manufacturing and economic activity takes place, wages have recently been rising at least 15 percent each year. Some jobs go unfilled. The one-child policy (in place until 2015) has led to a plateauing of the labor force.

Other costs, such as real estate, have also risen sharply. Chinese exporters are beginning to feel a squeeze between (i) rising costs and (ii) the falling RMB conversion value for the dollars or foreign currencies they earn.

Is the RMB still undervalued?

By massively appreciating their currency after 2005, the Chinese succumbed to Western government pressure. While many economists aver that the yuan (RMB) is still undervalued, they agree that in 2016 it is not undervalued by much.

Figure 2b shows that the huge 40.6 percent devaluation of the early 1990s massively undervalued the yuan and accomplished its purpose of making China the world’s leading exporter of manufactured goods. But since 2005, steady appreciation of the RMB led to its regaining the ground it had lost since the 1990s, as Figure 2b illustrates. Add to that wage inflation in the 2005–2016 period (based on the plateauing of the labor force because of the one-child policy), and several economists no longer consider the yuan to be undervalued.

Why pick on only China when other nations also “influence” their currencies?

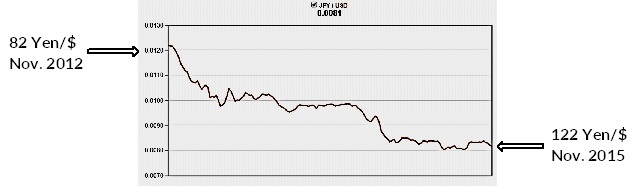

Indeed, if one were to search for a more egregious recent example, it would be the Japanese yen, which was consciously devalued by the Shinzo Abe government by around a third since November 2012.

Figure 4: The yen-per-dollar exchange rate fell in the period November 2012–November 2015 (Source: Oanda.com)

One of the Abe government’s top priorities on taking office was to drive the yen downward (devalue it) from a historically high overvaluation of 80 yen/$ (at which rate few Japanese exporters could make any money) to a more devalued rate of 124 yen/$ by 2015 (when Japanese exporters could make profits). The math is simple. At 124 compared with 80 yen/$, each dollar earned by the Japanese exporter converted into 55 percent more yen.

In retrospect, it seems astonishing that so many Japanese governments prior to Abe’s allowed the yen to remain at an overvalued rate of 80–100 per dollar, which not only grossly dampened Japanese exports, but also put the economy into the doldrums for so many years. Most economists would agree that at around 100–115 yen/$, the yen would be appropriately valued—in other words, that 80 was too high and that perhaps the 124 yen/$ at end 2015 is a tad too low. At any rate, the Abe government’s actions have jump-started the Japanese export engine and restored a plethora of Japanese exporters to profitability.

But is this not also a case of currency manipulation by the Japanese? And, as noted above, the IMF reports that more than half of the world’s governments have a hand in influencing or adjusting their exchange rates.

Conclusion

Why then pick on only the Chinese, especially if—with rising costs inside China—the 2015–2016 exchange rate of 6.2–6.5 RMB/$ may be approaching an appropriately valued rate?

Donald Trump, please read this post.

![]()