© 2020, Farok J. Contractor, Rutgers Business School

Featured Image Source: Wall Street Journal

This is a pre-copyedited draft version of an article to be published in Management & Organization Review. The final authenticated version will be available online at Cambridge University Press.

For at least 35 years, US politicians and pundits have scared the public with tales of declining vitality in US manufacturing, from Trump tweeting that “China is stealing our jobs”[1] to a recent article by a ranking congressman (Yoho, 2019) claiming that “America has lost its competitive manufacturing edge and the jobs that go with it.”

Such assertions are questionable at best and bunk at worst. Economic data do not support the claim that US manufacturing is in decline or that globalization and offshoring are the main culprits. The US remains a dynamic, innovative manufacturing nation, with productivity (in terms of output per worker) way ahead of any other nation. Moreover, until 2011, the US was the biggest manufacturing country on the planet (by total value of manufacturing output), and even in 2018/19 it remained a close second to China, with $1,867 billion in manufacturing output compared with China’s $2,010 billion. Figure 1 shows the US output index in current dollars at a record high.[2]

Figure 1: US Manufacturing Output, Current Dollars (Index 2012 = 100)

It is true, however, that the number of jobs in US manufacturing declined from a peak of near 20 million in 1979 to below 12 million in 2010 (recovering a bit to over 13 million workers in 2019), as shown in Figure 2.

Figure 2: Employment Numbers in US Manufacturing

The physical evidence is not hard to miss in the US “rust belt” states where hulks of abandoned factories blight the landscape. The approximate seven or eight million reduction in total manufacturing workers was accompanied by a downward squeeze on wages. Laid-off workers found other jobs, but at significantly lower pay. Diseases of despair, such as addictions and suicides, skyrocketed in the post-2008 period. By 2015, the “American Dream,” which for two centuries suggested that children would be better off than their parents, came to a crashing halt. By 2015, Pew Research found that “[j]ust 37% of Americans believe that today’s children will grow up to be better off financially than their parents” (Stokes, 2017). The disaffected then voted for nativist candidates, like Trump, who laid the blame entirely on globalization, particularly targeting China.

But Are Globalization and Offshoring the Real Culprits?

No. Globalized competition has indeed been responsible for some fraction of US job losses (in both manufacturing and services), as well as the angst it caused in parts of the US and Europe. But the seeming contradiction between the historically highest dollar value of US manufacturing output (Figure 1) and a workforce that had sunk to below 12 million workers by 2015 (Figure 2) can be explained by the increase in automation (including robotics), as well as in information and communication technologies (ICT) that enable more output with fewer workers — in short, enhanced productivity.

When a company faces downward price pressure from its competitors, eventually it must do something to cut costs in one of four ways: (1) offshore its production to lower-wage countries; (2) automate its equipment, thereby reducing the workers needed but making the surviving workforce more productive in terms of output per worker; (3) computerize and digitize its processes; and/or (4) cut workers’ wages. Offshoring is only one, besides other factors — (a) automation, (b) ICT, and (c) the shrunken bargaining power of labor versus management and shareholders — that jointly explain the transformation in US manufacturing.

The principal explanation for the phenomenon (seen in Figure 2) whereby the number of jobs in US manufacturing has declined (since the 1950s), while at the same time output has increased, is likely to be automation and ICT. Tellingly, the share of manufacturing employment in all (non-farm) employment — the dark-red line in Figure 2 — has been on an inexorable decline since the 1940s, when globalization was only a glimmer in the futurist’s eye. Hence, globalization could hardly have been a strong causal factor until perhaps the 1990s or 2001, when China joined the WTO.

In terms of output, US manufacturing remains an important part of the economy. According to Ramaswamy et al. (2017), manufacturing accounts for 70 percent of US R&D, 60 percent of exports, and 55 percent of patents. But because of the faster growth of the services sector in GDP, manufacturing contributed toward only 12 percent of US GDP and only 9 percent of employment in 2020. As Autor et al. (2015), Jaimovich and Siu (2019), and Michaels et al. (2014) indicate, it is very difficult to disentangle the causal effects of globalization from the effects of automation and ICT. In fact, some of the findings imply a larger causal role of automation and ICT. Moreover, I propose below another underlying factor — the declining power of unions in the US and the consequent shrinkage in manufacturing wages.

Hypothesis: Productivity (Aided by Automation and ICT) Are Dominant Explanations (Compared to Offshoring)

A comparison I did a few years ago,[3] illustrated in Figure 3, puts the US way ahead of any other nation in terms of productivity measures: “$ Output per employee per year,” as well as “$ Value added per employee per hour.” Not much has changed since then in terms of a comparison across the selected countries. US manufacturing should remain the envy of the world today. Alas, unrivalled productivity is the result of the willingness of US companies to replace a worker with a robot or new equipment, which means (1) layoffs of unskilled workers and (2) to some extent higher wages for the surviving skilled workers who, being better paid than their laid-off counterparts, increase income inequality.

Incidentally, in Figure 3 we see China coming out on top in one productivity measure, the ratio of $ Value added per worker divided by the $ Wages paid. But that is because the denominator — Chinese wages — was so low[4] compared to US and European wages, labor supply in China being 118 million manufacturing workers, compared to only 11.9 million in the US.

Figure 3: Productivity in the US versus Other Countries

Reduced Bargaining Power of US Workers

There is no law of economics or management that determines what share of a company’s profits should accrue to workers, versus management, versus shareholders. That is a function of unionization and bargaining strength.

A company’s profits has five claimants: (1) The government (taxes), (2) shareholders, (3) management, (4) workers, and (5) society. While (1) above is an exogenous variable, the distribution of after-tax profits accruing to (2), (3), (4), and (5) is indeterminate and is an internal decision made by upper management, which, reports suggest, has been paying itself and shareholders more, to the detriment of the share of the pie captured by workers.

Union membership in the US economy has sunk from 32 percent of the workforce in 1950 to around 10 percent in 2020, shown in Figure 4, with an accompanying reduction in bargaining power, although companies are more profitable. There are no counterfactual studies of how much greater the share of the labor force in after-tax profits would have been, had its bargaining power not been beaten down, particularly over the last four decades.

Figure 4: Percentage of US Workers That Are Members of Unions

Conclusions and Fodder for Further Research

There is nothing wrong with US manufacturing, which was at record output levels until January 2020 and remains vital, innovative, and the most productive (vis-a-vis output-per-worker) in the world. But in other ways, the US economy and its politics have gone through some wrenching transformations, such as the decline in manufacturing jobs and the depressed earnings of the bottom half of the workforce. Politicians, and the public that “follows” them, have seized upon globalization — specifically, the offshoring of work to low-wage nations such as China — as the chief culprit. Here I offer an alternative explanation: the likely larger role in job displacement played by automation, robotics, and ICT.

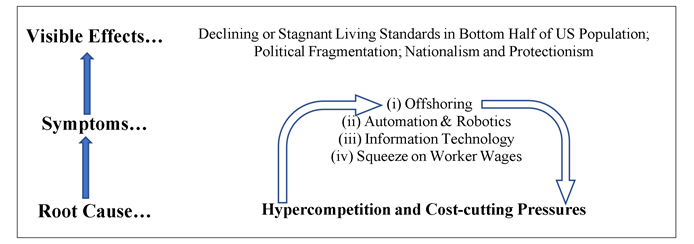

However, in my view, even the components of this alternative explanation — automation, robotics, and ICT –are actually the visible symptoms of an underlying root cause, namely hypercompetition. See Figure 5. In considerable part, competition results in downward price pressures. In turn, that forces companies to cut production costs under two broad strategic choices: (1) send production offshore and/or (2) automate with more “intelligent” machines that need fewer workers. Both result in layoffs, although less so under option (2). I hypothesize here that automation has resulted in far more US job losses than has offshoring. Conclusive studies are lacking, although we have weak evidence of this in Miller (2016), Jaimovich and Siu (2019), and Baldwin (2019). A third option also enables companies to reduce costs: (3) squeeze or reduce worker wages, given the weakening of union strength.

Figure 5: Root Cause, Symptoms, and Visible Effects

It is very difficult to empirically disentangle the relative impacts of offshoring, automation, and the worker share of after-tax profits, as Autor et al. (2015), Jaimovich and Siu (2019), and Michaels et al. (2014) have found.

But there is another research conundrum, to be candid, for economists and historians to probe: the mutually reinforcing feedback loop between offshoring and hypercompetition (Figure 5). Following the big reduction in tariffs under the Seventh GATT Conference, which concluded in 1979; the NAFTA treaty in 1995; China’s accession to the WTO in 2001; and the easing of business rules and liberalization of government regulations regarding incoming foreign direct investment (FDI) (World Bank, 2019; Contractor et al., 2020), companies found from the early 1990s a much more welcoming trade and FDI environment, enabling them to offshore more easily than ever before.

This raises a research question: How did competition in the US and Europe (the underlying cause indicated in Figure 5) intensify? Was it initiated by increasing shipments from domestic Chinese or Mexican exporters entering European or US markets, triggering an offshoring and automation response to meet the import threat? Or was the offshoring initiated by US and European multinationals themselves, who, after sensing heightening competition with each other, consciously established export-oriented FDI affiliates in China and Mexico to take advantage of lower labor costs and bring the cheaper output back home?

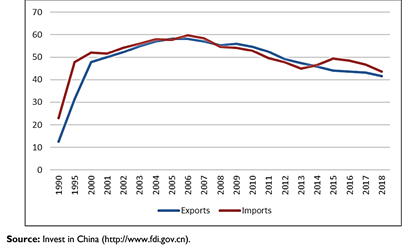

Figure 6 suggests a partial answer from a Congressional Research Service report that drew data from a Chinese Ministry of Commerce source. In 1990, the percentage of China’s exports done by foreign companies’ affiliates in China was only 12 percent. However, between 2001 and 2012, more than 50 percent of China’s exports were done by foreign companies. It was only from 2013 onward that domestic Chinese companies have accounted for more than half of China’s exports. This suggests that the mutually reinforcing feedback loop (illustrated in Figure 5) between hypercompetition and offshoring seeking cheaper labor costs was more the creation of US and European multinationals than that of local Chinese exporters. This requires further investigation.

Figure 6: Percentage Share of China’s Exports (and Imports) Done by Foreign Enterprises

At any rate, the broad conclusion of this article is that globalization (including offshoring) is only one symptom among several other corporate phenomena — such as automation, robotics, ICT, and wage reduction — that explains the resulting strains that have occurred in US politics and society.

++++++++++++++++++++++++++++++++++++++++++++++++++++++++++

REFERENCES

Autor, D. H., Dorn, D., & Hanson, G. H. (2015, May). Untangling trade and technology: Evidence from local labour markets. The Economic Journal, 125(584): 621–646.

Baily, M. N & Bosworth, B. P. (2014, Winter). US manufacturing: Understanding its past and its potential future. Journal of Economic Perspectives, 28(1): 3–26.

Baldwin, R. (2019). The globotics upheaval: Globalization, robotics, and the future of work. Oxford University Press.

Bartash, J. (2020, January 31). Share of union workers in the U.S. falls to a record low in 2019. MarketWatch.

Contractor, F. J., Dangol, R., Nuruzzaman, N., & Raghunath, S. (2020, April 20). How do country regulations and business environment impact foreign direct investment (FDI) inflows? International Business Review, 29(2), 101640.

Contractor, F. J. (2012, August 7). 7 Reasons to expect US manufacturing resurgence. YaleGlobal Online.

Goos, M., Manning, A., & Salomons, A. (2014, August). Explaining job polarization: Routine-biased technological change and offshoring. American Economic Review, 104(8): 2509–26.

Jaimovich, N., & Siu, H. E. (2019, November 7). How automation and other forms of IT affect the middle class: Assessing the estimates. Brookings Institution.

Michaels, G., Natraj, A., & Van Reenen, J. (2014, March 3). Has ICT polarized skill demand? Evidence from eleven countries over twenty-five years. Review of Economics and Statistics, 96(1): 60–77.

Miller, C. C. (2016, December 21). The long-term jobs killer is not China. It’s automation. The New York Times.

Morrison, W. M. (2019, June 25). China’s economic rise: history, trends, challenges, and implications for the United States. Congressional Research Service, Report #RL33534.

Price Waterhouse UK (2018). Will robots really steal our jobs? An international analysis of the potential long term impact of automation. PricewaterhouseCoopers LLP.

Ramaswamy, S., Manyika, J., Pinkus, G., George, K., Law, J., Gambell, T., & Serafino, A. (2017, November 13). Making it in America: Revitalizing US manufacturing. McKinsey Global Institute.

Stokes, B. (2017, June 5). Public divided on prospects for the next generation. Pew Research Center.

World Bank (2019, October 24). Doing business 2020. The World Bank.

Yoho, T. S. (2019, September 25). How America has lost its competitive manufacturing edge, and what can be done about it. Washington Times.

NOTES

[1] Trump, Donald J. [@realDonaldTrump]. (2011, September 28). China is stealing our jobs. We need to demand China stop manipulating its currency and end its rampant corporate espionage [Tweet]. Twitter.

[2] Even in inflation-adjusted terms, US manufacturing output in 2019 was near its 2007 high.

[3] Perhaps because of increased political sensitivity, the US Bureau of Labor Statistics (BLS) and the Bureau of Economic Analysis (BEA), who used to publish productivity comparisons for the US and other nations, stopped publishing this data after 2012.

[4] The RMB equivalent of $1.60 per hour was an “all China” average, including interior villages and provinces. By 2012, average wages in the eastern seaboard of China, where most of the country’s manufacturing takes place, had risen to around $4 per hour, which is still tiny compared to US and European wages.

Perceptive, well reasoned, and well documented. Great job.

LikeLike

Thanks, Tagi.

LikeLike